Let’s say you have a pretty good credit score. You always pay your bills on time, and keep your credit card balances low.

Then, you run into trouble. Perhaps you lost your job. Maybe you got sick? Or, you went through a divorce?

Whatever the reasons, you’re unable to make payments on your credit card. 30 days late. 60. Now 180 days late. Before you know it, the card is closed (charged off), and your credit score has tanked.

Naturally, you’re worried (and disappointed). You worked hard to preserve your credit score. A series of unfortunate incidents ruined it.

Don’t lose hope. There is a process through which you might remove charge offs from your credit report, and ultimately improve your credit score.

We are a team of credit attorneys. The process we’ve outlined below is how we address charge offs on our client’s credit reports.

You’ll want to take careful notes as you read this article. Addressing charge offs is a detailed-oriented, involved process.

What Is A Credit Card Charge Off?

First, it is important that we understand what exactly a credit card charge off is. Charge off is an accounting term, which refers to an account which the creditor believes is no longer collectible. Charged off debts are typically removed from the creditor’s balance sheet, for accounting purposes.

Under federal regulations, a credit card should be charged off after 180 days of delinquency. This means that you didn’t make your minimum payments on the card – 6 months in a row. This rule is pretty uniform, regardless of the company you’re dealing with.

An important point to understand: You still owe the debt on a charged off credit card. The fact that the creditor views the debt as unlikely to be paid, and treats it as a loss, does not mean that you no longer are obligated to pay it. You could be sued on the debt. We’ll talk more about that later.

A charged off account is closed. Needless to say, you can no longer use the credit card. After all, the credit card issuer wants to avoid losing more money.

How A Charge Off Impacts Your Credit Score

FICO scores are the credit scores used for 90% of lending decisions in the United States. These include buying a home, purchasing a vehicle, or obtaining a credit card. There are dozens of different versions of FICO. You can purchase your various FICO scores from MyFico

A single 30 day late payment can reduce a FICO score by as much as 100 points. If an account goes all the way to charge off status, that could drop your score by close to 200 points.

The better your FICO score is today, the more your score will drop if an account is charged off. Let’s use an analogy.

Suppose you have a new, white paint canvas. You throw a bunch of random paint, of many different colors, on the canvas. Those colors will be pretty prominent, as compared to when the canvas was just white.

Now, suppose you add just one more color to the canvas – a color which already appears on there. That color probably won’t be as recognizable, since you already had so many on the canvas.

If the charge off is just one of many bad items on your credit reports, it’s like the white canvas, which now has a bunch of colors. Since there are so many negative items on the report already, the charge off doesn’t stand out as much. It’s impact on your FICO score is more limited.

Now, let’s say the charge off is the only negative item on your credit reports. This is like a white canvas, which is splashed with a single, bright shade of red. It is very noticeable. The charge off will have quite a large downward impact on your FICO score.

Another thing to understand: The older a charge-off is, the less impact it has on your FICO score. In this sense, charge offs are like most other negative credit items: The more time passes, the less it damages you.

This is especially true if you focus on building positive credit history, by paying other accounts on time. Over the years, the positive accounts can outweigh any negatives.

How Long Does A Charge-Off Remain On Your Credit Reports?

Charge-offs can remain on your credit reports for up to 7 years and 180 days after the date when you first missed a payment (i.e. went 30 days late). The date you first missed a payment is known as the date of first delinquency.

Suppose you stopped making payments on a credit card in January of 2016. That is your date of first delinquency. 7 years and 180 days (i.e. 7 years and 6 months) after that is July 2023. This means that charge off will likely stay on your credit reports until that date.

In some instances, you might be able to ask the major credit reporting agencies (Equifax, Experian and TransUnion) to exclude the charge-off, 3 to 4 months before it is scheduled to fall off your credit reports. This is known as an early exclusion.

Being Sued Over A Credit Card Debt

If you owe enough money on a charged-off account, and the account is recent enough, the credit card issuer could sue you for payment of the debt. If they win in court, you could have your wages garnished. The same is true of your bank account.

How much money do you typically need to owe, in order to risk being sued on a debt? This varies heavily, depending on where in the country you live. In some states, where credit card issuers can sue in small claims court, you could face a lawsuit over charge-offs as small as $700.

In states where such cases must be filed in state court (involving higher filing fees), the amount owed typically needs to be somewhat larger. In such states, you’ll typically need to owe at least $1500, for a credit card issuer to bother with a lawsuit.

Of course, any time you owe a debt, a lawsuit is a risk. These are only rough guidelines. If you owe a credit card debt, it’s often a good idea to settle the debt (more on that below).

How long can a credit card issuer sue you for? That depends on the statute of limitations in your state, for contractual debts (i.e. unpaid credit card charge-offs). The statute of limitations begins when you first miss a minimum payment on a debt (remember, that is the date of first delinquency), and lasts for at least several years after.

Statutes of limitations vary for each state. In Alaska, you can only be sued for 3 years after the date of first delinquency. On the other hand, in Rhode Island, the credit card issuer can sue for up to 10 years after the date of first delinquency. Most states have a statute of limitations between 4 to 6 years.

If you’re sued by a credit card issuer, they must take certain steps to inform you that you’ve been sued. This is known as service of process. Failure to properly serve the lawsuit can be grounds to have the case dismissed.

Most credit card debt lawsuits are resolved through a settlement. It is rare for these cases to go to trial. You’ll probably have to pay most of the amount that you owe, although in some cases, reduced settlements might be possible.

Debt Buyers: Who They Are & What They Do

When a credit card is charged off, the credit card issuer has two options. They can either collect on the debt themselves, or sell it to a third party company (known as a debt buyer).

Major debt buyers include Midland Credit Management, Portfolio Recovery Associates, LVNV Funding, and Cavalry Portfolio Services. These companies are massive operations, which collect on many millions of dollars of debts at any given time.

Debt buyers typically purchase charged-off debts for a fraction of the amount owed (typically 5 to 10 cents on the dollar). This means that a debt buyer might purchase a $2,000 charge off for $100 to $200.

Debt buyers have several ways they might collect on a debt. First, they can place the debt on your credit reports, which of course damages your credit score. They might also call and write to you, seeking payment of the debt.

Keep in mind that debt buyers, like all debt collectors, are bound by the provisions of the Fair Debt Collection Practices Act (known as the FDCPA). If they violate the FDCPA, you can sue them for damages and attorneys fees.

Debt buyers often take a more aggressive step: Filing lawsuits. This isn’t just an occasional practice. In much of the country, debt buyer lawsuits make up a very large share of the civil cases filed. Just as with lawsuits from credit card issuers, your bank account or wages can be garnished if you lose.

Just as with credit card issuers, the statute of limitations applies. The statute of limitations is based on when the original credit card was charged off.

There are a number of tactics to fight debt buyers. Debt buyers often cannot prove their ownership of the debt. They would thus not have the legal right to collect on the debt. If you properly assert this defense, you can have your case dismissed.

In some instances, a debt buyer might attempt to sue on a debt which is past the statute of limitations. This is typically a violation of the FDCPA, and can be grounds to sue the debt collector.

If you’re sued by a debt buyer, you should seek legal assistance. A local legal aid organization might be able to help, or you can find a private attorney through the National Association of Consumer Advocates.

Removing A Charge Off From Your Credit Reports

We now understand how charged off accounts work. How do you get charge-offs removed from your credit report? There are several strategies. These are tactics that we, as credit attorneys, use every day.

Was The Account A Product Of Identity Theft?

Identity theft impacts millions of Americans each year, causing billions of dollars in losses. If you’re one of those whose identity was stolen, the issue is much more personal. Resolving identity theft matters can demand considerable attention, and knowledge of the law.

If a charged-off account on your credit reports was opened without your consent, you’ve likely been a victim of identity theft. It is important that you deal with the issue as soon as possible.

Our suggestion is that you first visit identitytheft.gov. This is a free website / guide, created by the Federal Trade Commission, to help you deal with identity theft issues.

You should follow all of the steps, and review your recovery plan. This website will help you create an affidavit (basically, a sworn statement) which you’ll need later in the process.

Next, you’ll want to visit your local police department, to report what happened, and file a police report. While local law enforcement is limited in terms of what they can do to help you resolve the matter, it’s important that you document what happened.

You’ll also want to call each creditor in whose name an account was opened through identity theft. Inform them that this account was not opened by you, and offer to send over the affidavit and police report.

At this time, it is important that you freeze your credit report. This helps ensure that whoever stole your identity cannot continue to apply for credit in your name. You can temporarily lift the freeze if you need to apply for credit. You can freeze your reports by contacting the credit agencies.

After taking these steps, you’ll want to also write to each credit reporting agency, and inform them of any accounts which were a product of identity theft. You should send over your police report, as well as the affidavit you prepared.

You’ll also want to contact the credit card issuer for the cards, and send them the affidavit and police report. It is important that you take steps to correct the fraudulent accounts, as soon as possible.

What if an account which was the product of identity theft is not removed from your credit reports? You might have grounds to sue the credit reporting agencies, as well as the credit card issuer. After all, if an account is not yours, and you’ve properly conveyed this, why should your credit be damaged?

It’s quite common for identity theft accounts to not be removed. After all, the credit reporting agencies and creditors are notoriously sloppy when it comes to properly investigating consumer disputes. This is one reason why they’re sued thousands of times each year.

Where might you find an attorney to help with such a lawsuit? The National Association of Consumer Advocates (known as NACA) is perhaps the nation’s largest association of consumer rights attorneys. Lawyers must apply to be members of NACA, and meet the organization’s membership requirements.

NACA offers a directory which allows you to search for an attorney in your state. This can be a good resource. Avvo is also quite useful for finding an attorney to help with your case.

A Word About Credit Sweeps

In recent years, some unscrupulous individuals have coached consumers to file false identity theft reports. By doing so, they hope to remove negative accounts (like charge-offs) which were opened in a consumer’s name. This practice is known as a credit sweep.

Credit sweeps are illegal, and can result in criminal prosecution. In recent years, authorities have prosecuted credit sweep operations in Las Vegas, Miami and other cities.

Besides being illegal and unethical, credit sweeps are unnecessary. As we discuss below, there is a legal, ethical process to address charge offs.

See If The Credit Reporting Agencies & Creditor Violated The Law, Such That You Might Sue In Federal Court

Suppose that you did open the account in question. It wasn’t a product of identity theft. You’ll next want to see whether the credit reporting agencies and debt collectors have reported the account in a seriously innacurate way.

Inaccuracies which damage your credit, if not corrected, might entitle you to money damages. Also, your attorney’s fees will typically be paid for by the creditor and/or credit reporting agencies – meaning that you don’t have to pay your lawyer out of pocket. As part of a legal settlement with the credit reporting agencies and creditor, you can often have the account deleted from your credit reports.

The Fair Credit Reporting Act (known as the FCRA) is the federal law which governs credit reporting in the United States. The FCRA provides that if you believe an account is being reported inaccurately, you may dispute the account.

The credit reporting agencies must perform a “reasonable reinvestigation” of your dispute. If they fail to do so, and the error on your credit report remains, you might have grounds to sue.

How do you know whether you might have an FCRA lawsuit? Your very first step should be to consult with an attorney, and have them review your credit file. See whether they think the error on your credit report is serious enough to sue on, if not corrected.

As mentioned earlier, NACA and Avvo are both great resources for finding attorneys. Typically, it will be free to have an attorney review your credit file, and tell you whether you might have a case.

Normally, the attorney you work with will prepare a dispute letter, detailing the errors on your credit file. They’ll also typically attach proof of the error, so that there’s no ambiguity about what the issue is. Often, they’ll have you sign this letter, and perhaps even have you mail it off yourself.

After receiving your dispute, the credit agencies will contact the creditor who reported the account, and forward them your dispute. This is done through an online system known as e-Oscar.

The creditor will investigate the dispute, and report their results back, typically within 30 to 45 days. If they fail to respond to your dispute, the account will be removed from your credit reports. Under some circumstances, it can be re-inserted onto your credit file.

What if the error is not corrected? In these instances, the attorney you’re working with will probably prepare a similar dispute for the creditor, outlining the errors, and requesting correction.

The Basic Of An FCRA Lawsuit

If the error remains, your attorney will sue the offending credit reporting agencies and creditor in federal court. As long as they can show that the information on your credit reports was innacurate, and harmful to your credit profile, you’re entitled to damages. Damages can vary from $100 to $1,000 (if you lack concrete proof of how you were harmed) to much more (if you demonstrate you were denied for credit).

As mentioned earlier, a deletion of the erroneous account is also typically negotiated. Obviously, this helps your FICO score.

When dealing with credit card charge-offs, we strongly suggest that you first consult with an attorney, to find out whether there are lawsuit-worthy errors on your credit report. If you do have a case, you’ll be able to address the negative account, without spending your own time or money.

Removing Charge Offs Through The Credit Repair Process

Let’s say you have an account which was not the product of identity theft. You also consulted with an attorney, who doesn’t see any major credit reporting errors.

You voluntarily opened the account, ran into trouble, and had it charged off. Now, you’d like to remove it. How do you go about doing this?

Settling The Account

Lets say that the account was not sold to a debt buyer, and is thus still owed to the original creditor. Let’s also assume that you still owe money to the original creditor.

Should you settle this debt? In many cases, the answer is yes. Settling the debt helps you avoid a lawsuit, if the debt is within the statute of limitations.

Settling the debt also makes it easier to potentially remove from your credit reports. In fact, in most cases, we encourage our clients to settle a charge off, before we work on it.

How much should you settle the debt for? The older the debt is, the more flexibility you’ll enjoy in terms of settling. That is, a 6 year old charge off can typically be settled for less than a 12 month old charge off.

We suggest you offer around 30% of the amount owed on the debt. That is, if $1,000 was charged off, you should offer $300. See how the creditor reacts, and negotiate from there.

In most cases, you’ll end up with a final settlement for between 40% to 60% of the amount owed on the card. If you have multiple charged off credit card debts, it could make sense to have a debt settlement attorney assist you.

Settling An Account In Exchange For Having It Deleted

If you’ve researched credit repair online, you might have heard of the concept of “pay for delete.” This is where you pay a debt collector or creditor on an unpaid debt, in exchange for having the account deleted.

Pay for delete generally doesn’t work with credit card issuers. Why? Credit reporting agencies like Experian, Equifax and TransUnion restrict credit card companies (and others) from deleting accounts in exchange for payment.

The credit reporting agencies want the most complete credit reports possible. They believe that removing negative accounts, in exchange for payment, defeats this purpose.

A Word About Bankruptcy

If you have many charged off accounts, with large balances, it can be quite challenging to settle. In this event, you might want to consider bankruptcy. Bankruptcy is a legal process, through which your debts are resolved using your existing funds.

There are two major types of bankruptcies: Chapter 7 and Chapter 13. Chapter 7 bankruptcies stay on your credit reports for up to 10 years, while Chapter 13 bankruptcies should be removed within 7 years.

If you have a substantial amount of charged off debt, you may want to consult with a bankruptcy lawyer. Avvo and NACA are your best resources for finding a good one.

Disputing The Account With The Credit Reporting Agencies

Now that you’ve settled the account (and it has not been deleted), the process of removing the account begins. First, you’ll want to dispute the debt with the credit reporting agencies.

In your dispute, you want to inform the credit reporting agencies that you don’t believe the account is being reported accurately. For this reason you want them to investigate the account.

In most cases, the account won’t actually be deleted at this stage. Rather, you’re trying to build a case, which eventually will get you a deletion.

Please note that this letter should be sent by USPS certified mail. This way, if the credit reporting agencies don’t respond to the letter, you have proof that you sent it. They might have violated the law.

The letter should include your full legal name, your Social Security Number, and date of birth. You should attach to the letter a copy of your photo ID, as well as proof of your mailing address (i.e. a bank statement or utility bill). You should also list the account number for each credit account you’re disputing.

Below is a sample dispute letter. This is a good template to follow, for your initial credit dispute.

Please note that we send the same letter to each of the three credit reporting agencies where the account typically appears. If the account is only listed on one or two of your credit reports, you should only address it to those credit agencies.

Please also keep in mind that the name and address information we’ve listed below is just a sample. You’ll want to include your personal information, not what’s written below!

TransUnion

PO Box 2000

Chester, PA 19016

Equifax

PO Box 740256

Atlanta, GA 30374

Experian

PO Box 4500

Allen, TX 75013

Hello,

I am writing to you regarding an account which appears on my credit reports. I believe that this account might not be reporting in a fully accurate and complete manner. I would like you to investigate this account, and update / correct it accordingly.

My name is Jessica Smith. My address is 1234 Sunny Street, Sunnytown, TX 12345. My Social Security Number is 123-45-6789. I was born on 1/8/1990. I have attached a copy of my photo ID, as well as my electricity bill for 1234 Sunny Street.

The account I’d like you to investigate is with Citibank, account #235983249. Please let me know what you find out, by writing to me at the address listed above.

Sincerely,

Jessica Smith

Send off this letter by certified mail. Wait 30 to 45 days, to see what comes back.

You should set aside each response from a credit reporting agency, in a safe, secure area. If you have a scanner, consider saving these responses to your Google Drive or Dropbox account. You’ll need to refer to these letters soon.

Disputing The Account With The Credit Card Issuer

After you recieve a response from the credit reporting agencies, you’ll need to see whether the account was in fact deleted. If it was not, you’ll need to contact the credit card issuer.

You should write to them at the mailing address listed on the credit report. In your letter to the credit card issuer, you should request a variety of information. This includes your full payment history on the account, and a copy of the application which led to the opening of the credit card.

At this stage, the objective is to obtain all information the credit card issuer has regarding your account. You want to confirm that the information they’re reporting to the credit reporting agencies is accurate and complete. More often than not, it isn’t.

To dispute with the credit card issuer, you’ll typically want to locate their address online, or from your credit report. You should also consider filing a copy of your letter with the Consumer Financial Protection Bureau, which is the government agency which regulates credit reporting agencies, credit card companies, and others. Complaints can be filed online, using the steps provided for in their website.

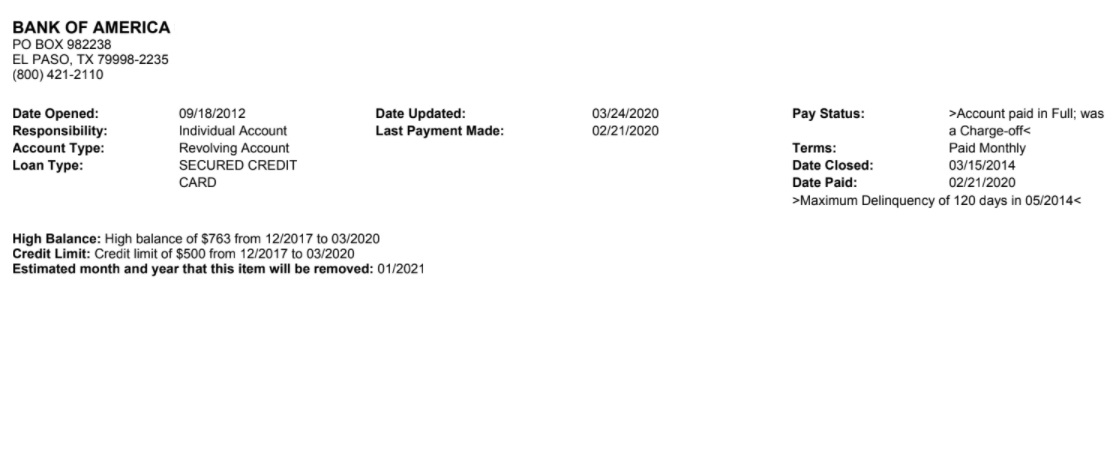

The Metro 2 Analysis

When you look at a charged-off account on a credit report, you’re seeing lots of data. The credit report will typically list the date the account was opened and closed, as well as the payment history on the account. You’ll also see things like the credit limit, status of the account, and more.

Below is how a typical TransUnion credit report appears, for a paid, charged-off credit card account. Please note that we have deliberately removed the account number, which would typically appear next to the name Bank of America. Please also note that our client provided his permission to share this document.

As you can see, there are numerous different fields of information which appear on your credit reports. In the first graphic alone, there are 16 fields of information. These range from the account name and number, to the payment status, type of account, date opened, date closed, and more.

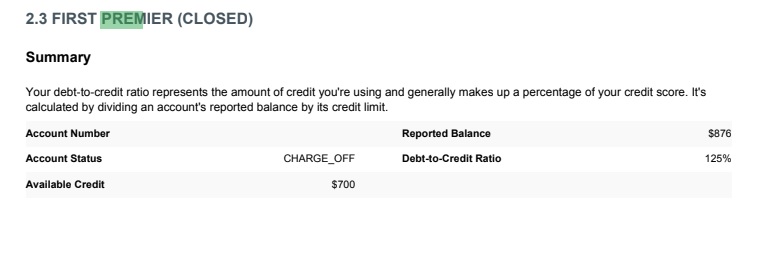

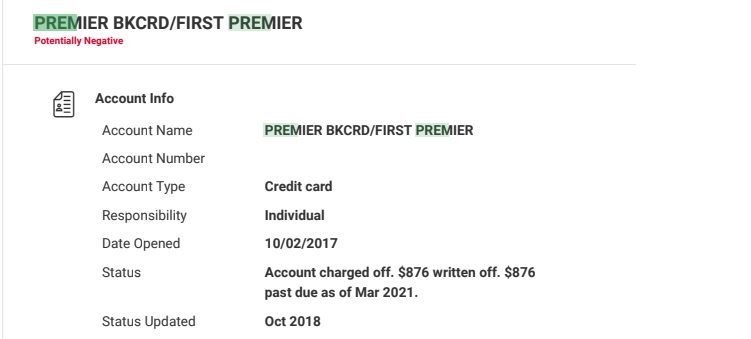

Now, let’s take a look at an Equifax credit report, for a different charged off credit card account. This client also provided her permission to share the account.

As we can see, the Equifax report lists many of the same fields as the Transunion report. Yet, we see some fields, like the Date of First Delinquency, which don’t appear on TransUnion. Additionally, we see that some relevant information (such as the High Credit and Date Closed) is left blank.

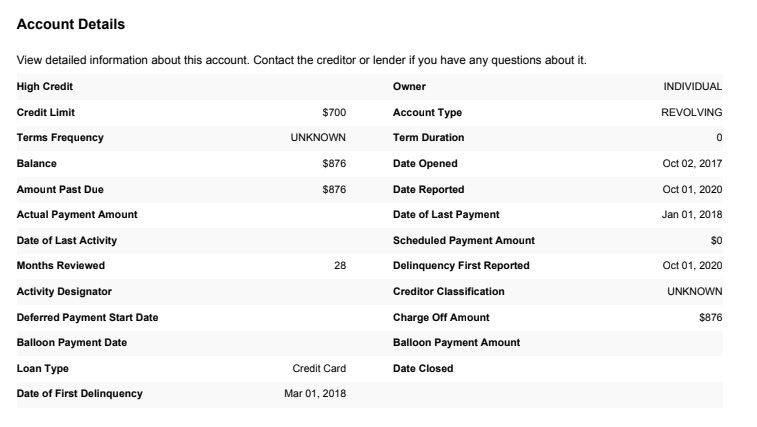

Finally, let’s take a look at an Experian credit report, for the same account.

We see that some of the same fields appear as with Equifax, while others don’t. For example, the Date of First Delinquency does not appear on Experian, and the date that the account was closed isn’t listed anywhere.

Please note that in the Experian report, we whited out the client’s account number. The Equifax report never even listed this information.

Why do all these fields of information appear on consumer’s credit reports? Credit reporting is supposed to follow the standards of Metro 2, which is the standard format for companies which are reporting information to the major credit reporting agencies.

Companies which report data to credit reporting agencies are known as data furnishers. Of course, credit card companies, such as the ones whose accounts you’re disputing, are one example of a data furnisher.

Here’s the reality: Data furnishers often don’t follow the requirements of Metro 2. The example above, where information is missing from the credit reports, is one very small example of this. Not following Metro 2 standards, particularly after you’ve pointed out the errors, can be a violation of the law.

Here’s the issue: Finding Metro 2 issues isn’t as simple as looking at a credit report, and examining which fields of information are present, and which are missing. You must understand how the overall structure of Metro 2 fits together.

The best way to learn all of this is by reviewing the Metro 2 manual, which you can find here. The manual isn’t light reading – it’s more than 200 pages long!

Metro 2 Dispute Letters

Once we’ve conducted a complete Metro 2 analysis, it is time to prepare the dispute letters. In each letter, you will outline the Metro 2 reporting errors, based on information which does not match, or which is incomplete.

You’ll want to send these letters to all three credit reporting agencies, and also file a CFPB complaint. You should also send this letter to the creditor, so that they’re on notice of the errors involved.

You’ve probably noticed that we haven’t provided a sample Metro 2 dispute letter. There’s a reason for this.

Metro 2 analysis varies, depending on which fields appear on the credit reports, which fields are missing, and so on. This isn’t a “one size fits all” approach in any sense.

Unlike the first round letter, each Metro 2 letter will be different, depending on the sorts of issues we’re focusing on. Therefore, using a template doesn’t make sense.

Arbitration; What You Need To Know

Let’s recap what all we’ve done so far. We’ve disputed the charged-off account with the credit reporting agencies. We’ve also disputed it with the credit card issuer.

Lastly, we’ve engaged in a Metro 2 analysis, with the credit reporting agencies and the credit card issuer. We’ve pointed out that various aspects of the account do not meet Metro 2 standards. The CFPB has been informed of all this.

At this point, you might think that you’ve done enough to have the account deleted. As reasonable as your assumption is, you’re probably wrong. Most times, credit reporting agencies and credit card issuers will simply verify that the account is accurate, and refuse to remove it.

Why go through all of this effort? Simply put, you’re setting up for the ultimate strategy to get this account deleted: arbitration.

Arbitration is a private legal process, where the parties which have a dispute appear before a neutral third party (known as the arbitrator). The arbitration is typically a retired attorney or judge.

Arbitration is an alternative to court, but it tends to operate less formally. Arbitration has long been favored by corporations, including most credit card issuers. Arbitration typically tends to cost less for them, and it eliminates expensive class action lawsuits.

In arbitration, the consumer (i.e you) will usually pay the filing fee (typically $200 or less). The business (in this case, the credit card issuer) pays all other fees. These include paying for the arbitrator’s time, as well as various case management and processing fees.

These fees, in total, typically run $4,000 to $5000, and can sometimes be even higher. This doesn’t include what the credit card issuer must pay to their attorneys. For these reasons, arbitration is often very costly for credit card issuers.

Most arbitrations are overseen by one of two major organizations: JAMS or the American Arbitration Association (known as AAA). The credit card agreement for the card you’re disputing, will typically state which organization will oversee the arbitration.

Which Credit Card Issuers Allow For Arbitration?

Whether or not you can arbitrate your claims with a credit card issuer, depends on the agreement you signed with the credit card issuer. You can find a list of credit card agreements on the website of the CFPB.

Most major credit card issuers have an arbitration clause in their agreement. These include Wells Fargo, Citibank, Discover, Synchrony Bank, Comenity Bank, First Premier, Credit One and American Express.

There are a few major credit card issuers which don’t provide for arbitration. These include Bank of America, Capital One and Chase. Note, however, that Chase has recently started to bring back arbitration for credit cards.

Filing Arbitration & Resolving Your Claim

If you want the arbitration to proceed, you must also pay the filing fee provided for in your credit card agreement. If the credit card agreement provides that the credit card issuer is instead responsible for this fee, then they must pay.

In most cases, you can file the arbitration, and pay the required fees a few weeks later. You can try to use this time to try to resolve your issues directly with the credit card provider.

Typically, AAA or JAMS will connect you (by email) with the attorney for the credit card company. This offers you the opportunity to detail the various ways in which the credit card issuer failed to follow their legal obligations.

With paid charge offs, you’ll often be able to resolve the case prior to arbitration. Remember that the credit card issuer has no claim against you, since the account is paid. Therefore, there is little to gain by going through arbitration.

Yet, they face the risk that you’ll take the arbitration forward – and win. Even if you don’t win, the credit card issuer has spent thousands of dollars on arbitration and attorney’s fees.

For these reasons, the attorney for the credit card issuer will often be willing to delete your account, in exchange for an agreement to cease the arbitration, and waive all of your claims. This is known as a mutual release agreement.

If the Metro 2 errors on your credit reports are serious enough (and you can tell a convincing story to the opposing attorney), you might even be able to obtain money damages. If you’re persistent, and educated on the law, this is possible.

Working With A Credit Repair Company

If you’ve read this far, you’ve probably realized that this is a complex process. If you’re willing to educate yourself, you could try to do this on your own.

On the other hand, it might make sense to have some professional help. One place to look is a credit repair company.

Full disclosure: Our team of attorneys runs a credit repair company, Tier One Credit. We want to state that upfront.

Questions To Ask A Credit Repair Company

If you’re looking into hiring a credit repair company, there are a few questions you should first ask:

1. What is the experience and expertise of this firm? That is, what qualifications do they have to serve as credit experts? Do they come from the mortgage lending world?

Perhaps they worked for the credit reporting agencies at some point? Or, are they attorneys? What we’ve detailed above is a highly involved legal process. So, why these folks? What do they know?

If you can’t find a convincing answer as to the qualifications of the company’s leaders, this should give you pause. You don’t want to spend your hard earned money on training a novice – or worse yet, throwing it away on someone who doesn’t know much and doesn’t care.

Looking up the company’s executives on LinkedIn and Google can be a good start to figuring out whether they’re indeed experts. Perhaps they share content on these platforms, or maybe YouTube?

2. What is their reputation? What do their customers have to say about them? Google Business and Yelp are good places to obtain this information. While it’s true that online reviews are subject to plenty of manipulation, you can also gain some insights here.

If you have a friend or family member who had a great experience with a credit repair company, that is an excellent indicator. The best companies have lots of raving fans, who spread the word.

3. What is their pricing structure? Credit repair companies usually have a few ways of charging customer.

Monthly Fees

The most common approach is the monthly fee model. Here, the customer is billed a recurring monthly fee, ranging from as little as $49 to as much as $250. The customer pays this fee each month, regardless of what results were delivered.

Some of these programs have a fixed time period, like 6 months. This means that the credit repair company will aim to complete work on your case within 6 months, and you won’t pay them after that.

Some of them also offer money-back guarantees. For example, if they cannot remove any negative credit items from your credit reports, within 6 months, they’ll give you your money back.

Pay Per Delete

Less common is the pay per delete model, where a company charges you only for what they are able to remove from your credit reports. If they cannot remove something from your credit reports, you will not pay them.

The advantage of this approach is that it’s more or less risk-free. You won’t be paying for results which you don’t see. Pay per delete companies often involve higher fees when you’re starting the service (anywhere from $200 to $400), and then charge per item deleted from each credit report (typically $50 to $100).

Your Rights As A Credit Repair Customer

If you sign up for credit repair services, you’re protected by the Credit Repair Organizations Act (known as CROA). This law restricts credit repair companies from charging you until services have been fully performed, and requires them to be honest in their dealings with you.

CROA also provides that a credit repair company must give you a written contract, which clearly states what services are being performed, and when you can expect them to be completed. You should carefully review any contract you sign, and hold the credit repair company to the terms of the agreement.

The Final Word

If you went through some challenges, and had credit card accounts charged off, you might feel like your situation is a bit hopeless. Yet, as you can see, there is a clear path forward. You can remove charge offs from your credit reports – either on your own, or with the help of a credit repair company.

Throughout this process, remember that you must be patient. It took 6 months for your account to end up charged off, and it’ll typically take at least as long to resolve it. Remain patient, focused, and determined. It will pay off.