Buying a home isn’t easy. You’ll need to figure out how much you’d like to spend on your new home (and how much you can afford). Often, these two numbers are not the same.

Then, you must provide a range of financial documents, which detail your income, assets, and much more. And of course, you’ll need to undergo a credit check.

There are many myths and rumors surrounding mortgages and credit scores. It’s important that you know the truth. Let’s dive in.

1. There Are Special Types Of Credit Scores Used For Mortgages

There are nearly 50 different types of FICO credit scores. FICO releases updated versions of it’s credit scores every few years (for example, if you use the free credit scores offered by Discover, you are receiving FICO Score 8), as well as specialized scores for various types of lending, such as auto loans.

For mortgages, most lenders use the FICO Score 5 for Equifax credit reports, FICO Score 2 for Experian, and FICO Score 4 for TransUnion credit data. These versions are known as Equifax Beacon 5.0, Experian/Fair Isaac Risk Model V2SM, and TransUnion FICO Risk Score, Classic 04.

Mortgage lenders want the most complete data possible. For this reason, they consider your credit reports and scores from all three credit bureaus.

While the exact differences between various versions of FICO aren’t entirely clear (since the credit scoring algorithms are a secret), many analysts believe that FICO mortgage scores give more weight to late payments, and other negative credit items,than newer versions of FICO. Therefore, if such items appear on your credit reports, you’ll want to explore having these removed through the credit repair process.

2. Your Mortgage Interest Rate Is Decided By Your Credit Score

Your mortgage FICO scores are the main factor (really, the only factor) in deciding the interest rate you’ll pay on your mortgage. The most competitive interest rates are available to those with a credit score of 760 or higher.

On the other end, for conventional mortgages, you’ll typically need a FICO score of at least 620. For government backed FHA loans (which are popular with first-time home buyers), you’ll normally need a FICO score of 580 or higher. For VA loans (which are designed for military veterans, or active duty service members), there are no minimum credit scores, although most lenders will ask for a score of at least 580 to 620.

The thing is, it’s not just about qualifying for a mortgage, with the minimum credit score possible. Rather, it is important that you get the best interest rate possible.

With higher interest rates, the numbers add up, costing you tens or hundreds of thousands of dollars, over the life of the loan. As your credit score decreases, you are essentially giving money away to the bank, for little reason.

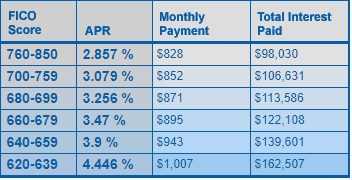

Take a look at the chart below, generated using the loan calculator from myFico. This displays the monthly payments for a mortgage of $200,000, with various credit scores and interest rates. As you can see, a lower credit score costs you every month, and thousands of dollars over the years.

Interest Rates & Monthly Payments – $200,000 Mortgage

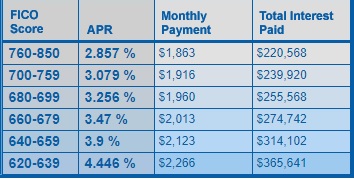

Now, let’s run the analysis if you’re buying a somewhat more expensive home, with a mortgage or $450,000. Clearly, a weak credit score is even more costly, when you’re spending more on a home. It should now be clear why your credit scores are so important, when purchasing a home.

It is important to note that your interest rate does not affect how much you can borrow; that’s determined by your income, assets, and debts. However, at any given borrowing amount, if you have strong credit, you’ll pay the lowest amounts possible, which allows you to save (and invest) more of your money, further growing your wealth.

3. Lenders Use Your Middle Credit Score

As we’ve noted, mortgage lenders pull all three of your credit reports, and obtain a FICO score for each credit report. However, contrary to popular belief, lenders don’t average credit scores.

Rather, they use the middle of your three credit scores. Let’s suppose that your Experian mortgage FICO score is 710, while your TransUnion score is 690, and your Equifax score is 680. Lenders will use the TransUnion score (690), to decide the mortgage rate they’ll offer on the loan.

4. Lenders Use The Lower Mortgage Score Amongst Joint Applicants

As noted above, for a single borrower, most lenders use the middle score, to decide your mortgage interest rate. What if you are borrowing with your spouse or partner? Or, for that matter, any other co borrower?

Lenders will take the middle score of each borrower, and use the lower middle score. Suppose that you have mortgage credit scores of 720, 713 and 702. Your spouse has scores of 700, 680 and 675.

Your middle score is 713, while your spouse’s is 680. Your mortgage interest rate will be decided by the lower score, that is, your spouse’s score of 680.

As you now from our earlier discussions, this will almost certainly mean a higher interest rate. For this reason, it is very important that both parties have strong credit; otherwise, your great credit will mean very little, if it isn’t supported by a similar score for your spouse.

The Final Word

Mortgages and credit scores can be quite a confusing topic. However, if you’re educated, you can obtain the best rate possible. If you’re looking for more information on how to improve your credit scores for a mortgage, you might want to check out this piece.